THE REPORT

WEEK OF AUG 8, 2026

Week of August 2-8, 2026

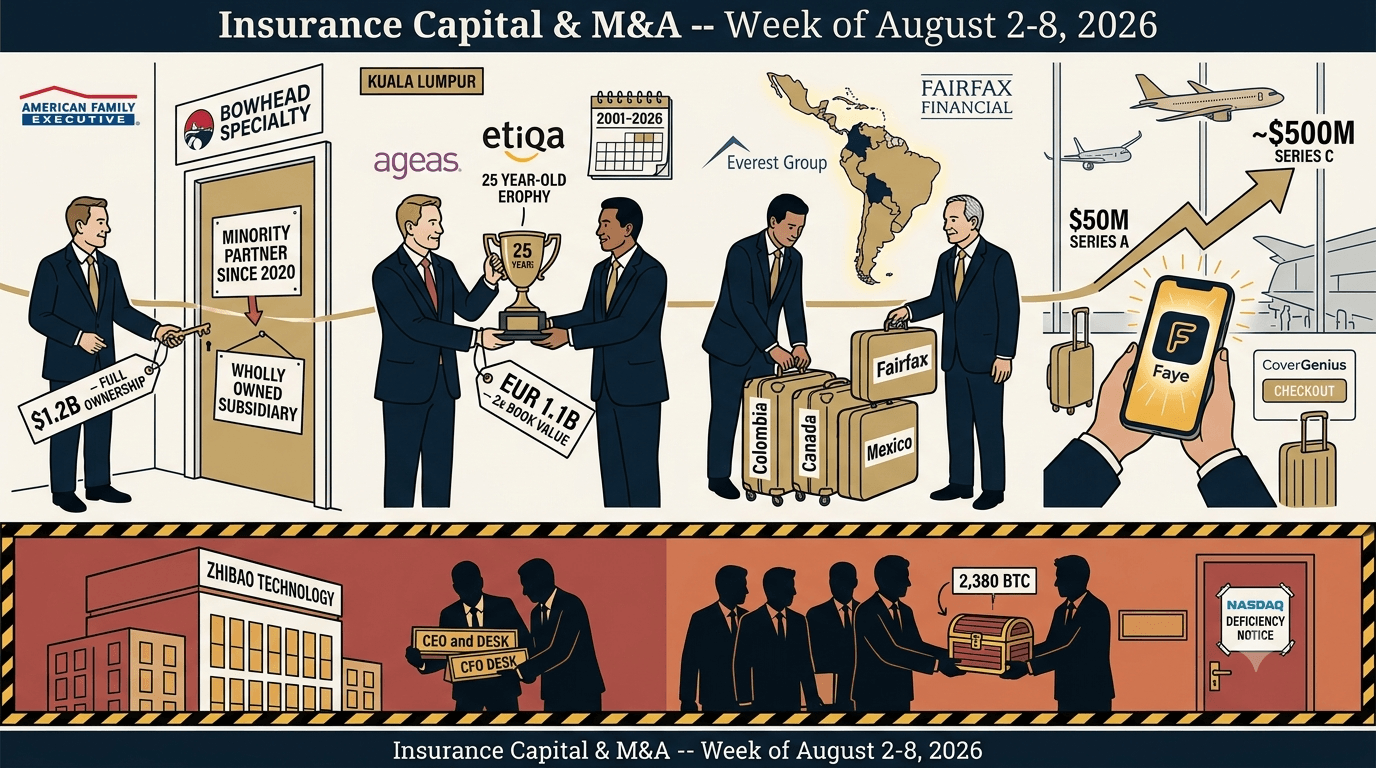

$2.35B+ in disclosed capital | 4 primary transactions + 3 special situations | American Family takes full ownership of a specialty insurer, Ageas exits a 25-year Asian joint venture, Everest completes its third retail divestiture, and an AI travel insurance platform triples its valuation

Read this week's report

Read this week's report THE PODCAST

EPISODE 165

Yagub Rahimov, Founder & CEO of Polygraf.ai

Founder & CEO, Polygraf.ai · AUG 4

The Problem Is Not the Technology. It Is the People Using It.

EP 164 — Jon Kelly — CEO, Modern Metric JUL 24

The Man Who Built InsurTech Before It Had a Name

EP 163 — Jonathan Crystal — Founder & Managing Partner, Crystal Venture Partners JUL 17

We Talk Too Much About Technology and Not Enough About People

EP 162 — Justin Levine — Co-Founder & CEO, Shepherd JUL 10

The AI Race Moved to the Construction Site. Shepherd Is Building the Insurance for It.

EP 161 — Cheri Martinen — Managing Partner, OneDigital JUN 29

The Filing Cabinet Nobody Fixed — And the AI Liability Gap Nobody Is Talking About

EP 160 — Curtis Barton — CEO, ALKEME JUN 22

You Can't Play the M&A Game If You're Not Growing Organically First

All 165 episodes → COMMUNITY

InsurTechLA lives here now

Nine years of meetups & fireside chats, folded into one brand. The archive — and what's next.

CAPITAL and M&A

From Seed to Exit

Capital formation and sell-side or buy-side M&A via BMI Capital International (FINRA/SIPC).

ADVISORY

Strategic Advisory

Market intelligence, and ecosystem access.

The week's deals, decoded. Every Sunday.

Subscribe free

Panel moderation and keynotes at InsureTech Connect, InsurTech Insights, and industry

conferences since 2016 — engagements →